[ad_1]

THE assessment of corporate governance practices and disclosures by all public-listed companies, real estate investment trusts (Reits) and business trusts in Singapore has been conducted on an annual basis for the last 15 years. Beginning as the Governance and Transparency Index in 2009, the assessment framework was revised and renamed the Singapore Governance and Transparency Index (SGTI) in 2016. The framework has remained essentially the same since then, apart from minor revisions made to reflect some of the changes in the Code of Corporate Governance.

Recent changes in the Singapore corporate governance landscape pointed to the need for a more thorough revision in 2024. These changes reflect both global and local trends.

Globally, we have seen the incorporation of sustainability concerns into corporate governance. The traditional shareholder-centric view of corporate governance is being widened to cover a broader range of stakeholders. In seeking to achieve long-term firm value, corporate leaders are increasingly considering not only profitability and productivity, but also social and environmental issues.

Governance also drives sustainability. Progress in sustainability is more likely in companies with well-functioning boards that have incorporated sustainability issues into their oversight responsibilities.

Locally, there has been an effort to professionalise directorship. The Singapore Institute of Directors (SID) has introduced the SID Director Accreditation Programme to develop directors in eight foundational competencies identified in the SID Director Competency Model: governance, director duties and practices, financial proficiency, risk management, strategy development, digital proficiency, human capital, and sustainability fundamentals. The programme also allows for training in specific areas tailored to board roles and organisation type, as well as for ongoing director development.

In response to these changes, the SGTI framework was revised for the current assessment round. Governance continues to be the mainstay of the revised framework, but it has been supplemented with indicators assessing the fundamentals of sustainability reporting such as materiality and sustainability governance.

BT in your inbox

Start and end each day with the latest news stories and analyses delivered straight to your inbox.

In addition to having more environmental, social and governance (ESG)-related indicators, sustainability issues also have greater weight. The “Engagement of Stakeholders” pillar of the framework has been renamed “ESG and Stakeholders”, and its weightage increased from 10 per cent to 20 per cent.

Besides these changes, the structure of the index remains unchanged. It has a base score and an adjustment for bonuses and penalties. The base score continues to have five sections (which together make up the acronym BREAD): Board Responsibilities (35 points), Rights of Shareholders (10 points), ESG and Stakeholders (20 points), Accountability and Audit (10 points), and Disclosure and Transparency (25 points). The maximum achievable score is 143 points, comprising 100 points for the base score and 43 points for bonuses.

The framework takes reference from the SID Director Competency Model, allowing for the evaluation of whether certain director competencies are reflected in corporate disclosures and practices.

The revised SGTI is designed to be a dynamic index, with greater flexibility to align with changing regulatory requirements. Recent years have seen a number of new Singapore Exchange listing rules, addressing issues such as independent directors, the remuneration of chief executive officers, climate change and whistle-blowing. It is likely that this will continue, as sustainability reporting matures and is standardised.

Allowing for these changes to be incorporated into the assessment framework more frequently will be another feature of the SGTI moving forward.

Overall results: A size effect exists

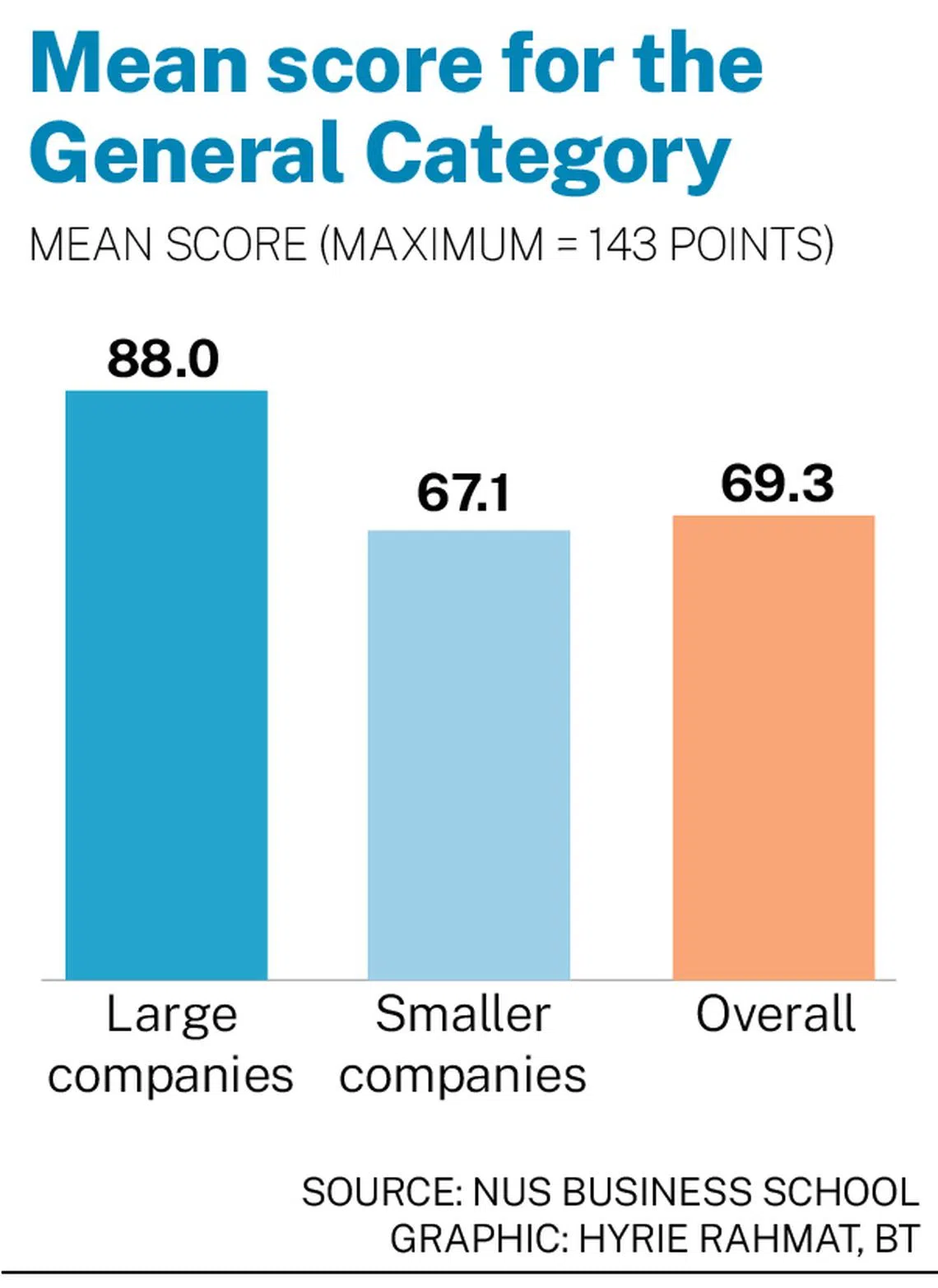

The SGTI 2024 had a mean score of 69.3 points. Although the changes in the framework are such that meaningful inter-year comparisons are not possible, the revision has resulted in a drop in the overall mean score. This is due to the removal of questions that had disclosure rates reaching, or close to, 100 per cent because of mandatory compliance, and a stricter standard of assessment applied to remaining questions given the maturing of the market. The inclusion of more sustainability questions also contributed to this drop.

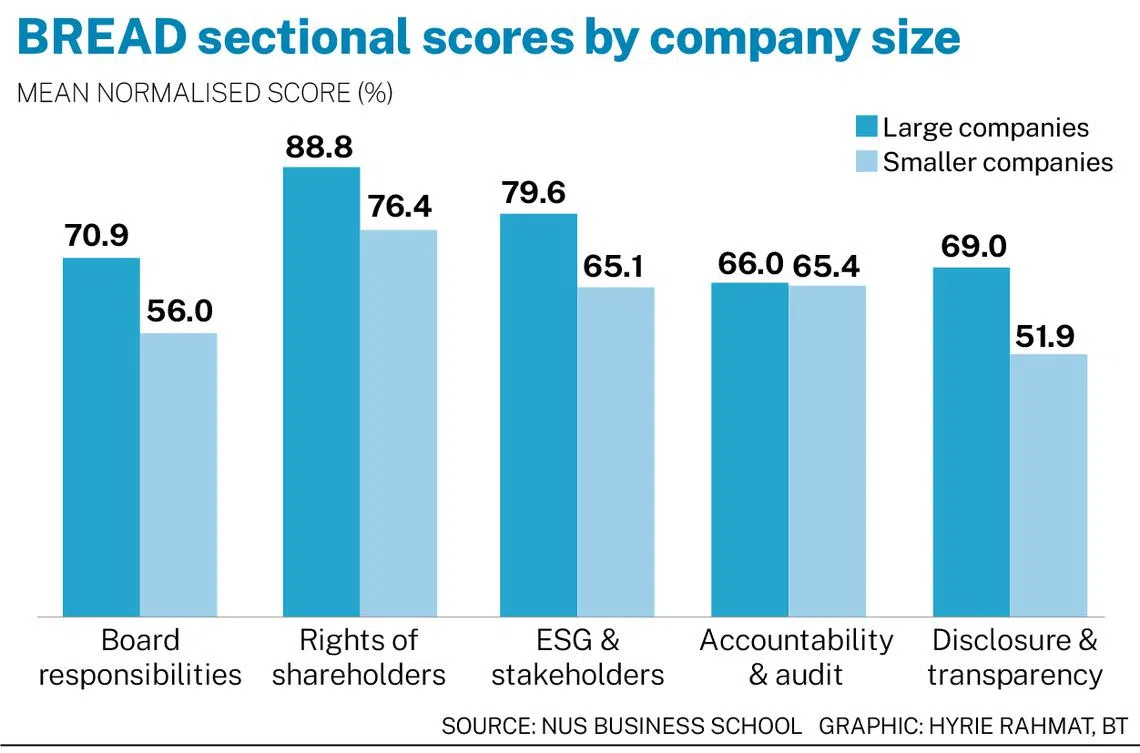

The SGTI assessment framework is based on five dimensions (see “How scoring for the Singapore governance index is done”). Companies show the strongest performance in disclosures relating to shareholder rights (mean normalised score of 77.7 per cent), followed by sustainability-related matters (66.6 per cent) and accountability and audit (65.5 per cent).

A clear size effect can be seen between large companies (having a market capitalisation of more than S$1 billion) and smaller companies (market capitalisation of up to S$1 billion). The latter have a mean overall score which is 20 points less than that of the large companies.

The size effect can also be seen in the various dimensions of corporate governance. The largest difference is in the mean normalised scores for Disclosure and Transparency (69 per cent for large companies versus 51.9 per cent for smaller companies, a 17 percentage point difference).

Similarly, in the areas of board responsibilities and sustainability, large companies have a 15 percentage point advantage in the mean normalised score (70.9 per cent versus 56 per cent for Board Responsibilities; and, 79.6 per cent versus 65.1 per cent for ESG and Stakeholders). The only dimension where such a size effect is not seen is in Accountability and Audit (mean score of around 65 per cent for both large and smaller companies).

Sustainability reporting: Attention needed on smaller companies

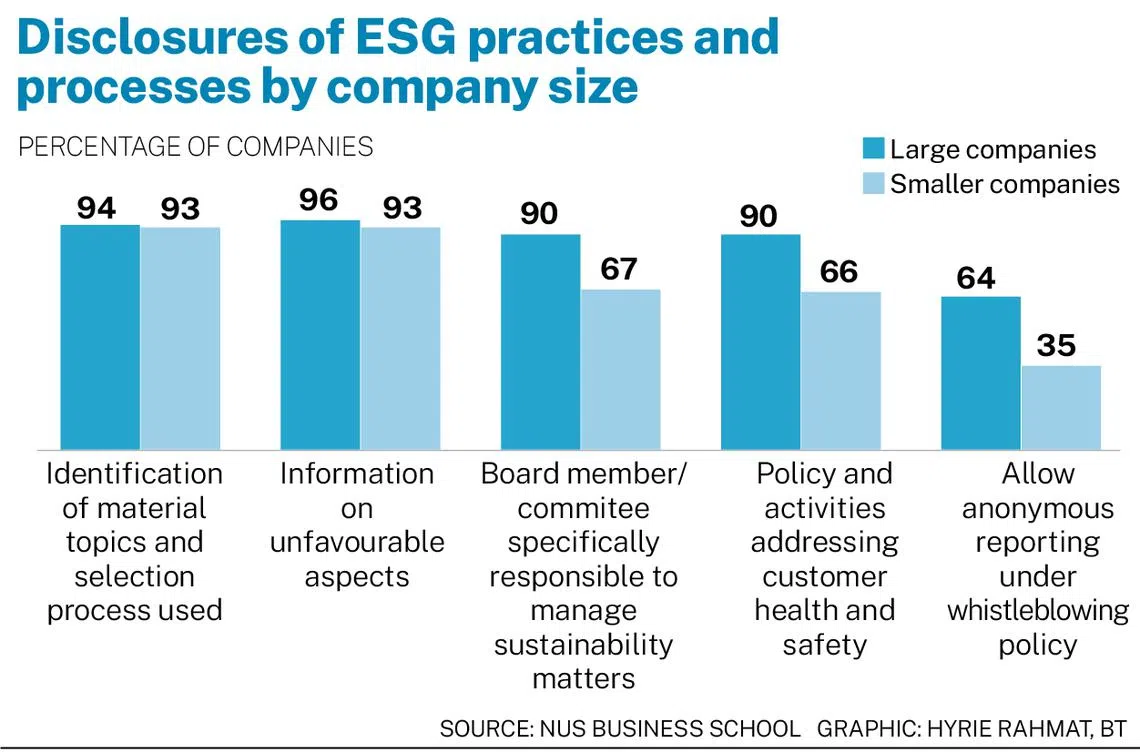

Smaller companies have made progress in the fundamentals of sustainability reporting such as materiality. Almost all listed companies, regardless of size, have identified their material topics, along with their selection process and the reasons for selection (around 93 per cent for all companies).

Similarly, there is little size differential in the disclosure of sustainability-related information that is unfavourable to the company – one aspect of addressing greenwashing. Among smaller companies, 93 per cent make such disclosures, versus 96 per cent of the large companies.

In areas such as sustainability governance however, large companies have a clear advantage. Ninety per cent of large companies have a board member or a board committee specifically responsible for managing sustainability matters, versus only two-thirds of the smaller companies.

A size differential can also be seen in specific ESG topics. Disclosure rates of companies’ policies and activities regarding their efforts to address customer health and safety are 24 percentage points lower for smaller companies than for large companies. Similarly, disclosure of the provision of anonymous reporting for whistle-blowers is 29 percentage points lower for smaller companies.

The results of SGTI 2024 show that one way to raise the standard of sustainable corporate governance disclosures across the market is to raise the performance of smaller companies. Encouraging progress can already be seen in the basics of sustainability reporting, such as materiality disclosure.

Further improvement could be accomplished by providing support, targeted to areas in which they still lag behind large companies. This would cover board responsibilities and sustainability broadly, and, specifically, matters such as sustainability governance and greater protection for whistle-blowers.

Such support, together with the raising of disclosure standards, would help to improve smaller companies’ transparency and accountability, along with their prospects for long-term sustainability and success.

Indeed good governance and sustainability should not be the sole domain of large companies.

Lawrence Loh, Nguyen Hanh Trang and Annette Singh are respectively director, research analyst and senior research associate of the Centre for Governance and Sustainability at the National University of Singapore Business School

[ad_2]

Source link